As a homebuyer, the term “Flood Factor” isn't completely known or accepted, but I predict that within five years, everyone will know about it. From the Risk Factor website: “A property’s Flood Factor, Fire Factor, and Heat Factor indicate its comprehensive risk from flooding, wildfire, or extreme heat ranging from 1 (minimal) to 10 (extreme). Flood Factor considers flooding from rain, rivers, tidal, and storm surge to determine the risk of water reaching the building over a 30-year period.

Currently, major real estate websites like Redfin and REALTOR® have fully adopted Flood Factor as a critical feature of understanding property values. It's really just a matter of time before it becomes commonly accepted information. With the increased temperatures causing increased rain flow velocities, and the incredible volume of natural disasters occurring in the past couple of years, people will be more sensitive to purchasing homes in flood zones. Looking into these factors will become very important in the future as the climate changes.

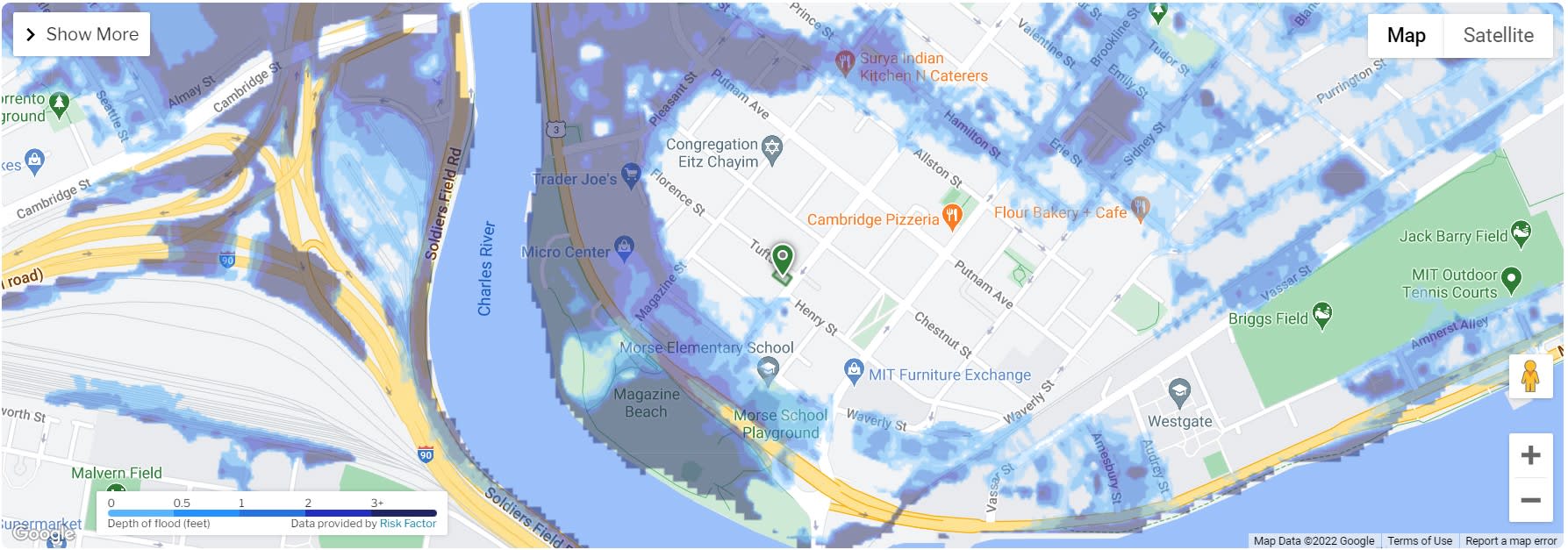

Let’s take a closer look at the Flood Factor system: a home with a score of 1 out of 10 is the most favorable rating. When searching for homes, besides using MLS, I highly recommend using Real Estate Agent and Redfin because they incorporate Flood Factor into their apps. I recommend that you look up the Flood Factor for every property you are considering and make sure you're comfortable with the rating and the description on the website about what that rating means. Specifically, scroll down far enough to look at the shaded blue/purple map to get a better visual and read their analysis of the flood zones and risks of the neighborhood your home is in. Make sure you're okay with not just the rating, but also how the house looks on the shaded satellite map on the website. Even if it's a 1/10, you might not be comfortable with that rating if you're just 10 feet away on all four sides from a shaded flood zone.

You can also zoom out from the property you’re researching to see that in general, to stay in Cambridge or whichever city you are looking at, you may have to compromise and accept some level of flood risk. There's definitely less risk closer to Central Square/mid-Cambridge and parts of Cambridgeport, but you'll see a lot of shaded areas in desirable neighborhoods too. If you’re looking to buy in only one particular city, it’s best to familiarize yourself with the shaded map of the city to see which areas, if any, have a higher or lower flood risk.

You also want to look at the surrounding flood dynamics. With the surrounding flood dynamics, it's easier to guess if the flood zone is due to the potential of the ocean rising and thus backing up the Charles River, or due to a particular house being in a low-lying area. My personal rule of thumb with Flood Factor is it's fine to be in a zone with a rating that’s higher than a 1 out of 10, but I would want to have a rating that’s at least average or better than average for that particular neighborhood or town.

For example, a Flood Factor of 6 out of 10 is okay in Cambridgeport or Back Bay, but that same rating may be too high for somewhere like Belmont, where most of Belmont is a 1. To me, there’s no point in buying a 6 out of 10 to live on a standard street that doesn't get you anything special. Something special would be like a waterfront property, where you have to be willing to pay the cost of being in a flood zone in order to get something nice.

A common question I get is: “This house has a Flood Factor of 4 (just an example, but this can be any number over 1). Should I be concerned?” Unfortunately, it’s not a simple yes or no answer. Instead, I’d ask, “Is a location desirable enough and are there enough other 4’s in that area that people will still want to buy it?” Also, “Are you compromising on the Flood Factor because you get something really special? Is it waterfront property?” In other words, when I think about the flood dynamic, I think about whether there's something beneficial about a location to warrant buying something with a Flood Factor over 4. For example, you may consider a 6/10 for a house in Back Bay, but not for a house in Arlington.

In general, I would never advise a client to buy a 4/10 in the suburbs since there's no benefit to one particular lot compared to the rest of the town. There's absolutely no reason to risk flooding or future flood insurance fees in the suburbs. Also, I would never buy waterfront property that’s on the sandy ground by the ocean. Near the North Shore and in Maine, where it's all huge granite rocks, I would buy something on granite that's at least 20 feet above sea level. Sandy ground also erodes away and your house can end up in the water. This happens on Cape Cod and Plymouth often. The ocean erodes away the sand and a lot of these houses that used to be 100 meters away from the ocean are now IN the ocean.

At some point, Flood Factor ratings will impact property values, if they haven't already. Right now, the Flood Factor isn't fully recognized by the buyer market. However, my prediction is that at some point in the next 5-10 years, FEMA will start to base their flood zone insurance policies on scientific models like Flood Factor, whereas currently, they’re using antiquated FEMA maps. FEMA maps are arguably antiquated since they originated decades ago, and then incrementally adjusted while accommodating budgetary and political pressures. This is evidenced by seeing direct waterfront condos in Revere having the lowest flood risk in FEMA maps while having a higher flood risk in Flood Factor. If and when FEMA adopts a more modern mapping system, insurance will likely be required for many homes that don’t currently require it. And with increasing awareness of global warming and rising waters, having a higher flood factor rating will hurt the value of the property on resale.

In the future, homebuyers need to be aware of the existence of Flood Factor and to consider the information related to Flood Factor as they decide on which properties to offer, so get ahead of the curve and start getting acquainted with it now.