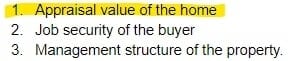

Finance contingency, also known as a mortgage contingency, is comprised of three main issues to consider when looking at how the bank determines whether a home purchase is financeable or not:

- Appraisal value of the home

- Job security of the buyer

- Management structure of the property.

I’ll address each of these three dynamics below and discuss the risk of waiving each dynamic.

Appraisal value of the home

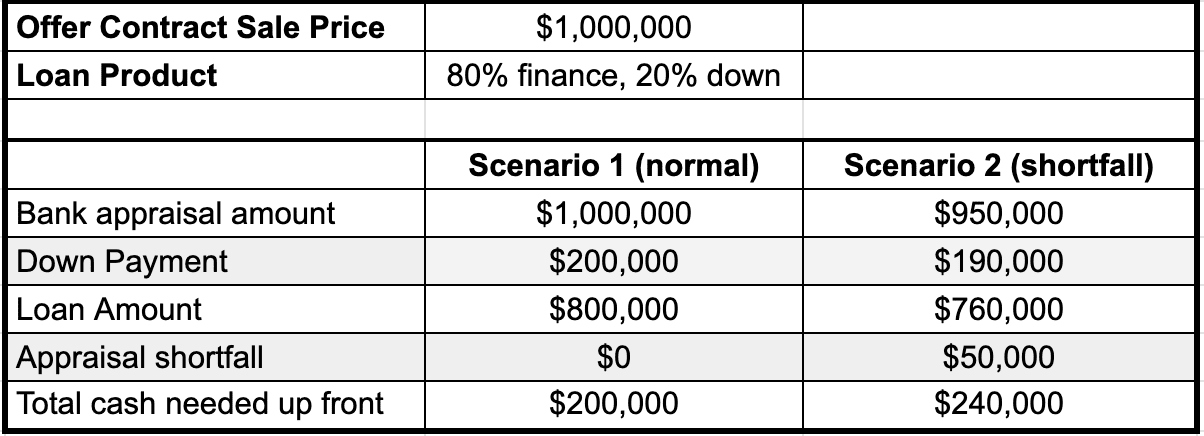

When discussing the appraisal value, this is the most common issue that comes up in the home purchase process: a lender will use terms like 80/20, 80/10/10, 95/5 and so forth to shorthand their basic products. These are percentages where the first number in the 80/20 shows how much is being financed and the last number is generally the down payment. If there’s a middle number, that’s the 2nd mortgage. These percentages are based off of the appraised value of the home and NOT the agreed upon sale price. For example, let’s say you agree to purchase a home for $1m, but the bank appraisal comes out to $950k, the 80/20 product means the bank is only willing to loan you 80% of $950k. See illustration below:

The risk here is that if you waive the appraisal section of the mortgage contingency, you could be on the hook for coming up with enough cash to cover the appraisal shortfall. In this example, it would be an extra $40,000 cash.

One way to mitigate the appraisal issue is to use a local lender that has the ability to use high-reputation appraisal companies. Sometimes, if you use an out of state loan officer from a nationwide bank, you might end up with an out-of-town appraiser that doesn't know the difference between property in Harvard Square and a property in East Somerville. They might be accustomed to operating in subdivisions that are forty miles outside of town, where two miles of distance doesn't have much variation in pricing.

What you should do is to work with a loan officer from a local bank with a good reputation to make sure you can get a loan, while still waiving the mortgage contingency. Some loan officers are very conservative in a positive way and just want to make sure that they’re not wasting anyone’s time or energy. They want to make sure right from the start that a particular buyer is a sure-thing for closing, thus making them the best kind of loan officer to work with. The fact of the matter is, with this type of loan officer, they will brush you off without a thought within two seconds if they don’t think they can lend you money. I know it sounds rude but it’s the best for everybody in the end. The reality is that with less successful loan officers, tend to reach more for more business. This means they will be overly optimistic and are keeping their fingers crossed that everything works out, and even lead the buyer on only to let them down at the end.

Keep in mind that the bank appraisal generally has less fidelity than a real estate agent’s valuation. Real estate agents are trying to find a very technical market value, whereas bank appraisers have a bit more flexibility and their job is to make sure the bank isn’t making a mistake in taking on a huge risk. This means that if a bank appraiser can hit the contract sale price, they absolutely will, as long as it’s within the bounds of the standard appraisal guidelines and licensing rules. Now don’t get me wrong, I believe the bank appraisal is still completely valid. Fundamentally, market value is whatever a buyer is willing to pay for a property, barring any unique connections and relationships like a parent selling a house to a child for $1, or a grateful parent paying a few extra dollars for their son’s university fencing coach’s home. For more information about home valuation, take a look at my entry on Appraising a Home for Buying or Selling.

Job security of the buyer

The second thing a bank looks at is your job security. Having confidence that you can cover the monthly mortgage payment is paramount to making sure you don’t default on your mortgage. Regular income from a steady job is so important that you can have one million dollars in your bank account and still not qualify for a mortgage, no matter how small. Or let’s say that you just graduated from school and started a new job two months ago. You likely still can’t get a mortgage unless you can build up 1-2 years of work history. Banks do release products periodically where certain professions are viewed as lower risk--that’s why you might hear about physician loans from some of the larger banks where a person who has a signed job contract to start as a physician or has just started work as a physician can qualify for a mortgage based on their current salary without regard to past salary. These products come and go, so it’s important to look around if the first bank you contact doesn’t carry one.

Keep in mind, for the purposes of this article, the connection between waiving a mortgage contingency and losing one’s job has nothing to do with whether the buyer can actually pay the mortgage or not. The issue is that the bank will no longer provide the mortgage if the buyer loses their job before closing. The risk here is that if you waive the mortgage contingency and lose your job, you’ll have to figure out a different way to secure the money to buy the house otherwise you lose your earnest money. In many cases, the earnest money is 5% to 10% of the price of the house. In the million dollar house example above, you’d be losing $100,000.

The need to find a different way to secure money to buy a house without a traditional mortgage is the most common dynamic when finding a co-signer, usually a parent or relative. Less common methods include getting a portfolio loan or using hard money. The latter options are risky and usually only done when a person has plenty of money to cover the purchase, but are choosing to leverage themselves for other investment purposes or if it’s a house flipping situation where the buyer knows they’re going to be able to sell the property again in a few months at a profit.

Management structure of the property

Lastly, the bank wants to make sure that nothing in the ownership structure of the property could negatively affect the value of the house, which is mostly relevant with condo associations. For example, if a condo association has poor financials or one person has too much control, this will negatively affect market value and will give a bank pause and cause it to lower their valuation or worse, not allow financing at all. The management structure of a building is generally analyzed via the condo questionnaire, which is a fairly standard list of questions produced by the lender and filled out by a trustee of the association. The lender’s attorney will also review the condo documents and financials in addition to the questionnaire to ascertain the health of the association on behalf of the lender.

An example of too much control within an association might be if in a ten unit building, one owner owned three units. That means one person has the equivalent of three peoples’ votes and that really waters down the averaging effect of multiple units. Say for repairs the condo docs for this ten unit building require a majority vote, then that one owner of three units only needs three other owners to agree with them. In a two-unit association, an eccentric owner could kill the long term exterior maintenance budget if they insist on complete historical accuracy in the woodwork and paint. Alternatively, in a three-unit association, if a cheap absentee landlord owns two out of three units, the building is guaranteed to be maintained at a bare minimum level and possibly even below the level of safety codes.

Rental restrictions have historically also impacted mortgageability dynamics. If a building doesn’t allow any rentals at all, that devalues the potential sale prices since it removes any flexibility at all for military or career oriented people that might get transferred out of town. If a building is 100% rented out, that also makes it less valuable since owner occupancy generally improves the safety and maintenance levels of a building. Generally, banks like to see high owner occupancy without any rental restrictions. Depending on the economic climate, a bank might have a restriction where a building needs to be at least 50% owner occupied in order for the buyer of a unit to qualify for a loan.

One last example of management health is the question on every lender’s questionnaire about whether the condo association is facing any litigation. Litigation doesn’t automatically mean the association is bad, but it definitely means the association could lose some money since even a completely frivolous lawsuit can cost the defendant tens of thousands of dollars.

The risk of waiving your mortgage contingency with this dynamic is that you’ll have to go with a portfolio loan. This isn’t terrible if it’s the only part of the mortgage dynamic you don’t qualify for. You still have your income and if the appraisal came out well, there are a number of banks that will still finance the property just under slightly higher interest rates or using ARMs.

Conclusion

Some experts will say that a buyer should never waive their mortgage contingency unless they have the cash to cover the price of the whole property. My opinion is that it really kind of depends. The home buying process does have other risks besides the mortgage and inspection. For example, buyers are always taking a risk that they are buying the wrong property, especially in the city where one house can vary drastically from another house on the same block. Choosing the wrong house might even be a larger risk than waiving the mortgage contingency, especially if with cursory due diligence, the three main categories above present to be low risk. Whenever there’s a market downturn, there are thousands of property owners in Massachusetts that lose 25% or more of the value of their home, and hundreds that end up foreclosing and losing all their equity. The risk of waiving a mortgage contingency is around 5% of the value of the property, since you only lose the deposit. Alternatively, the risk of not buying in a market-steady neighborhood can cost 7-figures in lost opportunity. I’m not saying that one should assume risks left and right—I just want to put the various risks involved in purchasing a home into perspective. If what I’ve discussed sounds like a daunting task with all the variables, I don’t blame you! I encourage you to consult your broker to help determine if this is something that you should be considering before you put your offer on a house.