What a year so far! We’ve definitely seen a return to vacationing and international travel this summer after everyone basically lifted all their COVID restrictions. It’s been great to gather with family and friends with similar comfort as we did pre-2020.

Inventory Analysis

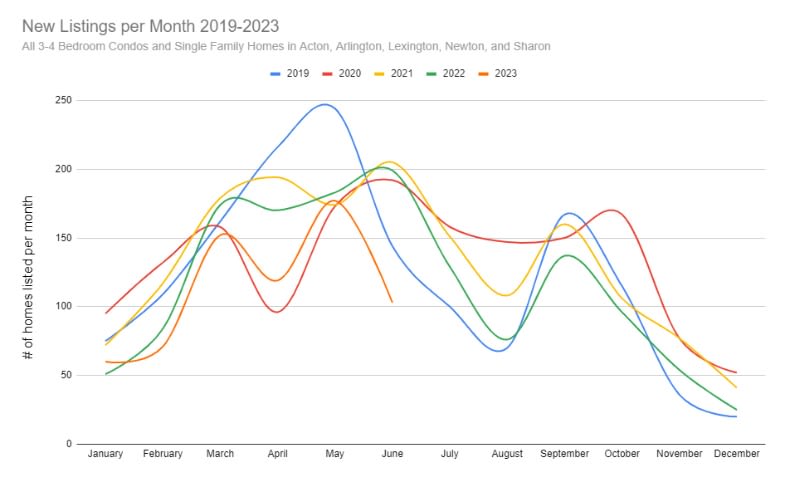

For our spring 2023 market recap, I decided to conduct an analysis on inventory. I compared new listings data across 2019 through mid-July. To get a representative sample of the most competitive markets, I picked a sampling of towns with highly rated schools and limited the properties to 3-4 bedroom condos and single family homes. The chart below shows the data of when homes were newly listed. Note that I did not include any data for properties that expired, but I did include all properties that were active and under contract today. What this means is that the actual June/July 2023 data would be even lower than shown below since it’s possible that some listings today would expire tomorrow, but I don’t believe that would affect the general trends we see.

To see the original file, click here for the google sheet. I’ve set privileges to view only, so feel free to copy the file if you want to play with the data.

2019 is a representative curve of the pre-pandemic market, with the large spike in inventory happening late April into May. You can see that in 2023, the opposite happened–we saw inventory go up as usual after the winter holidays, then bottom out in April, only to again taper down for an early summer.

For an idea of overall annual inventory, see the following table. To make it comparable to this year’s data, I only tabulated homes listed through July 14 in any given year.

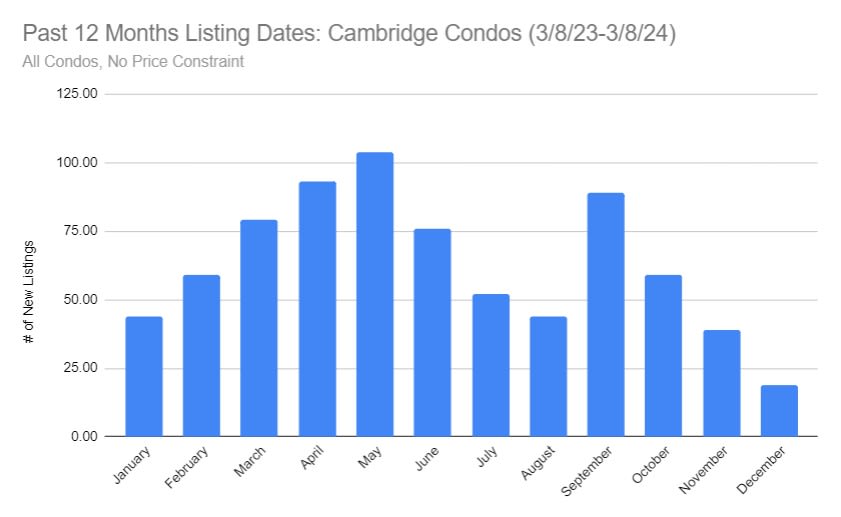

For a more urban example, I looked at Cambridge. For all condos sold in the same period, January 1 through July 14, we saw 288 condos sold in 2019, and 291 condos sold in 2023.

See also in Market Watch: Only a tenth of mortgages have an interest rate above 6% — that’s a big problem for the U.S. housing market.

Bidding War Examples

Here are some general examples of bidding wars we saw during this past 2023 spring market. Note that we collect a lot of data by directly calling listing agents at other brokerages. I’ve kept things fairly generic in order to maintain client confidentiality since some of this data comes from bidding wars Splice Realty agents have participated in and some have been shared by listing agents at other brokerages.

Properties listed below $1,000,000:

- Norwood 38 offers, all over asking, winning bid waived inspection contingency and was more than 25% over list price

- Malden 25 offers, all over asking, winning bid waived inspection and mortgage contingencies and was more than 15% over list price

- Lexington 10 offers, all over asking, winning bid waived inspection and mortgage contingencies and was more than 13% over list price

- Acton 17 offers, all over asking, winning bid waived inspection and mortgage contingencies and was more than 15% over list price

- Medford 14 offers, all over asking, winning bid waived inspection and mortgage contingencies and was more than 12% over list price

- Arlington 7 offers, all over asking, winning bid waived inspection and mortgage contingencies and was around 9% over list price

- Waltham 9 offers, all over asking, winning bid waived inspection and mortgage contingencies and was around 12% over list price

- Cambridge 13 offers, all over asking, winning bid waived inspection contingency and was more than 20% over list price

- Somerville 8 offers, all over asking, winning bid waived inspection contingency and mortgage contingencies and was more than 10% over list price

Properties listed above $1,000,000:

- Belmont 5 offers, all over asking, winning bid waived inspection and mortgage contingencies and was around 3% over list price

- Medford 5 offers, all over asking, winning bid was around 6% over list price

- Lexington 10 offers, all over asking, winning bid waived inspection and mortgage contingencies and was 30% over list price

- Lexington 24 offers, all over asking, winning bid waived inspection and mortgage contingencies and was around 25% over list price

- Arlington 5 offers, all over asking, winning bid waived inspection contingency and was more than 5% over list price

- Lexington 5 offers, all over asking, winning bid waived inspection contingency and was around 7% over list price

- Cambridge 6 offers, all over asking, winning bid waived inspection and mortgage contingencies and was more than 25% over list price

- Cambridge 1 offer, close to asking price

When will the market go back to normal? This is the million dollar question of course! Generally, I’m speculating 2025 will be the first year with close to normal inventories. Interest rates is a big part of the equation, but I’m not necessarily predicting interest rates to go down. If they do, then inventory will go up of course. But even if they don’t, the people that had to sell their houses starting when interest rates went up in 2022 will finally be used to the high interest rates and be willing to buy their long-planned next property and sell their current one. Over the years I’ve found that once people need to sell, they eventually will. Especially in groups where the urgency isn’t as dire, such as empty nesters who have flexibility on when to sell.

Another way to look at this is what I call the Minivan Theory. Minivans are clearly acknowledged to be the greatest form of transportation ever created. Yet inventories have always been sky high with minivans littering dealer lots, with the unknowing masses turning up their noses at this technological marvel. Pre-pandemic, you could buy a 301 hp AWD Toyota Sienna, for 12%-15% below MSRP. Today, you have to order from the dealer, and hope you get the chance to buy it at MSRP or higher before the dealer sells it to someone else at a higher price. This is why there’s inflation, and why the Fed is desperately keeping interest rates high. Once minivans are back in stock, then inflation will settle down, interest rates will lower, and the economy can go back to normal. Admittedly, my friends call this nuts, but the end predictions and conclusions are the same as those of professional economists.

With regard to inventories, there’s been a lot of great articles about why inventories are low. One of my favorites this year was this one, written by a loan officer in the Baltimore area. New construction housing has been rebounding really well, as evidenced by large housing construction companies having a breakthrough quarter and providing innovative solutions to bring monthly financing costs down for buyers. The lack of existing home inventory provides strong demand for new construction. That said, in our region, the lack of land available for new construction limits that market. There’s some movement nationally for abolishing single-family zoning. This NPR article discusses the tensions on both sides of the “missing middle” dynamic, and how a few states and municipalities are working towards having exclusive multi-family zoning. In the Boston area, the influx of thousands of high paying jobs is a large reason why inventories are low, since restrictive zoning limits additional housing units.